Korea’s $13 Billion Venture Market Has a Body Composition Problem

Last quarter, Korean venture investment hit ₩2.18 trillion ($1.6B) — up 34% year-over-year. AI captured 45% of all deployment. The government committed to its largest-ever capital injection cycle: ₩3,500 billion in…

Also available on 애당초 4개의 시선 (Ethan Cho: Four Lenses on Everything) on Substack.

Read on Substack →Last quarter, Korean venture investment hit ₩2.18 trillion ($1.6B) — up 34% year-over-year. AI captured 45% of all deployment. The government committed to its largest-ever capital injection cycle: ₩3,500 billion in fresh fund-of-funds allocation, a ₩7.45 trillion growth fund, ₩400 billion from the national pension, and a new retail venture investment channel (BDC) that went live in March.

[](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa3d99ebf-e70e-4443-86bd-222315950a2c_302x167.jpeg)

The headlines say: Korea’s venture ecosystem is thriving.

The body composition says something else.

The DEXA Scan

A DEXA scan measures what a mirror can’t. Not weight, but what the weight is made of. Muscle versus fat. The Korean venture market needs one.

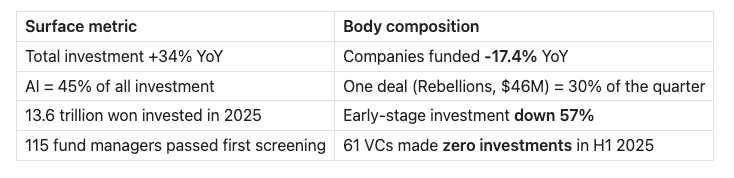

Here’s Q1 2026:

[](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa01c6935-a8ce-4a08-86c9-b0a6d992ef03_734x178.png)

More capital. Fewer companies. Larger checks into later rounds. The venture market is gaining weight while losing muscle.

How Government Capital Becomes GLP-1

GLP-1 drugs — Ozempic, Wegovy, the newly FDA-approved oral Foundayo — are the most successful weight-loss intervention in pharmaceutical history. They work. Patients lose 15-25% of body weight. The mirror looks great.

The problem: 30-40% of the weight lost is lean muscle. And a meta-analysis of 8,000 patients showed that when the drug stops, the weight comes back — but it comes back as fat, not muscle. The patient ends up with worse body composition than before they started.

Korea’s government venture capital operates on the same mechanism.

The Korea Fund of Funds (모태펀드) is the dominant LP in Korean venture — directly or indirectly backing the majority of domestic VC funds. When the government injects capital, total investment rises (looks healthier on the scale). But the intervention simultaneously crowds out private LPs, distorts GP incentives toward government allocation criteria rather than market returns, and creates structural fund-life constraints (8-10 year mandates) that make true seed investing economically irrational.

The National Assembly Budget Office’s own data confirms it: the fund-of-funds’ leverage effect on private capital mobilization has been declining since 2014. Same dose, less effect. Classic drug tolerance.

The government’s response? Triple the dose. In the last 24 months: a new BDC retail channel, a 63% increase in fund-of-funds allocation, and a ₩7.45 trillion parallel growth fund. Three simultaneous interventions into an ecosystem already showing tolerance.

What This Means for Allocators

If you’re a global LP evaluating Korea, the standard pitch is: “$13.6 billion market, government support, AI momentum, underpriced relative to the US.”

That pitch is technically accurate and structurally misleading. Here’s what to actually look for:

1. The GP bifurcation is permanent.

Large GPs now route through the National Growth Fund. Mid-tier GPs compete for the fund-of-funds. This creates two distinct species of Korean VC — and neither is optimized for what global LPs actually want (high-conviction early-stage with genuine alpha).

The GPs worth backing are the ones who *don’t* depend on government allocation. Ask any Korean GP: “What percentage of your LP base is government-linked?” If the answer is above 70%, you’re investing in a policy instrument, not a venture fund.

2. The AI concentration is a feature and a bug.

45% of Q1 deployment into AI sounds like conviction. Look closer: one semiconductor deal was 30% of the quarter. Strip out the top 3 deals and Korean AI venture drops to a modest allocation. The “AI boom” in Korean VC is actually 5-7 large checks, not a broad ecosystem shift.

The opportunity is *below* this layer — Korean AI startups at seed and pre-Series A that are invisible to government-funded GPs because the fund economics don’t support $200-500K checks with 10+ year horizons.

3. The exit infrastructure is the real bottleneck.

Korea has no meaningful tech M&A culture. Large corporates build rather than buy. The IPO pipeline is tightening with profitability requirements. There is no developed secondary market.

All the capital entering the system in H2 2026 creates portfolio companies that need to exit by 2033-2034. Into what? This is the question no government allocation announcement addresses. If you’re evaluating a Korean GP, their exit thesis matters more than their entry thesis.

4. The emerging manager window is now.

Precisely because the government-funded ecosystem is structurally oriented toward larger, later-stage, policy-aligned deployment — there is a genuine gap at the seed layer. The GPs filling this gap tend to be:

* Smaller (sub-$30M funds) * Independently funded (non-government LP base) * Sector-specialized (particularly in AI infrastructure and developer tools) * Operationally involved (not check-writing, but company-building)

These managers are hard to find through traditional Korean VC channels because they don’t show up at government allocation presentations. They show up in founder communities, open-source ecosystems, and cross-border networks.

The Framework: Execution, Decision, Responsibility

One lens we use to evaluate this market: when AI commoditizes Execution (code, analysis, operations), the value of venture capital migrates to two layers that cannot be automated — Decision (what to fund, when, at what terms) and Responsibility (fiduciary duty, board governance, LP accountability).

McKinsey’s 2026 AI Trust Survey, covering 500 organizations, arrived at the same conclusion independently: *“Agency isn’t a feature — it’s a transfer of decision rights.”*

[](https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F57b1b3cd-b8ed-42f7-979b-a335e764be9b_856x1055.png)

In a market flooded with government capital where Execution is cheap and abundant, the scarce resource is judgment. The GPs worth backing are the ones whose decision-making process — not their fund size or government connections — is the source of alpha.

The Takeaway

Korea’s venture market is not broken. It’s structurally medicated. The patient looks healthy on the scale. The DEXA scan tells a different story.

For LPs considering Korea exposure: look past the headline numbers. Ask about body composition — early-stage pipeline, private LP co-investment ratios, exit infrastructure, GP independence from government allocation. The opportunity is real, but it lives in the muscle, not the weight.

---

*This is a part of an occasional series on Korean venture market structure for international allocators. If your allocation committee is evaluating Korea, I’m happy to share the underlying data.*

*Ethan Cho is based in Seoul and writes about venture capital, AI, and cross-border market structure. Previously at Google, Samsung, and Qualcomm.*